Mr. Cross taught me so much valuable knowledge and helped me build my financial skills and portfolio.

I started with nothing, knowing absolutely nothing about investments, trading, or reading charts. But thanks to the amazing mentors at Blackstone, they taught me

everything I needed to know!

At Blackstone, I get to choose my favorite mentor and learn by following their personal strategies. Plus, I can also study with other top Blackstone mentors to expand my knowledge even more!

- All

- Markets

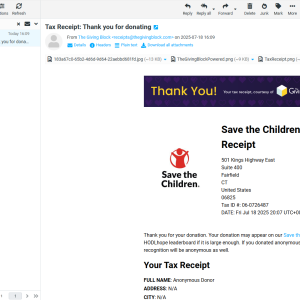

Dear Community Members,With heartfelt gratitude, We’re deeply grateful to share that Blackstone Community has officially donated the surplus income from the first half of 2025 to Save the Children, a globally recognized nonprofit organization.This donation fulfills our commitment under the “1% Surplus for Good” fund and was successfully transferred through the blockchain giving platform, The Giving Block.This is our way of putting our values into action:Investment isn’t just about returns...

Maxis Fully Upgraded, Blackstone Community Token Set to Launch: Ushering in a new era of financial technology and value consensus In July 2025, Blackstone Community will officially launch its community token (Token) public offering plan and list it on major cryptocurrency exchanges. This is not only a celebration of a technological upgrade but also a convergence of shared understanding and value consensus. This token issuance marks a pivotal...

Download Transcript Goldman Sachs’ Daan Struyven discusses how recent geopolitical events and evolving tariff policies are affecting the commodity and economic landscape.