The prospects for European stocks are brightening as the region’s fiscal spending rises, the economic growth outlook improves, and interest rates are poised to fall, according to Goldman Sachs Research. On a recent call, our analysts discussed the opportunities in the broader European equity market as well as for utilities, real estate, and food retailers.

What’s the outlook for the STOXX 600 index?

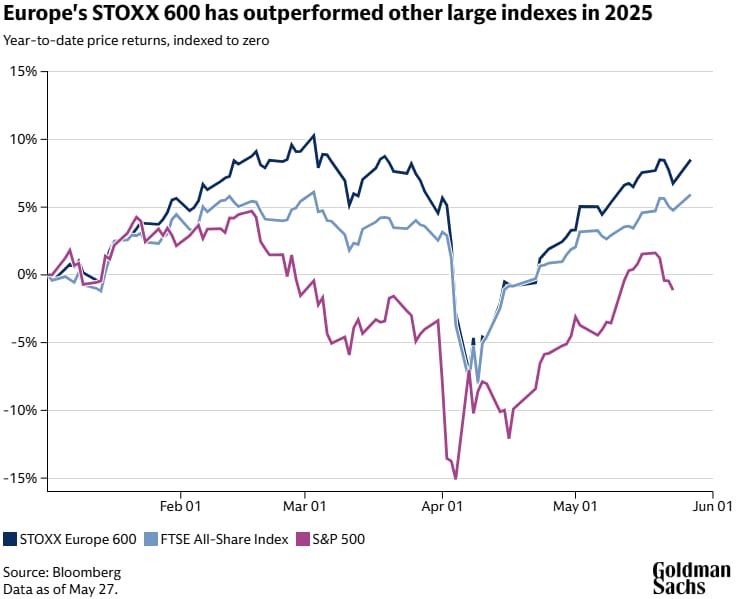

The STOXX 600 index of large European companies is up 8.5% so far in 2025 (as of May 27). Sharon Bell, a senior strategist in Goldman Sachs Research, says that the relatively low price of European stocks compared with their US counterparts may have contributed to this surge. The STOXX 600 is forecast to rise about 3.5% to 570 in the next 12 months.

European companies that sell to their local markets are in a particularly strong position, in part because they are less exposed to foreign-currency fluctuations, Bell says. “Domestic companies don’t have that dollar exposure, they have underperformed for a long period of time, and they are trading at a deeper discount,” she says.

Our economists expect the euro area economy to grow slowly this year — they forecast that the rate of real GDP growth at the end of 2025 will be just 0.9% (as of May 16). But Bell points out that the outlook for Europe’s economy looks set to improve in 2026 and beyond.

This improving outlook is partly down to policy, Bell adds. “Fiscal policy, defense policy, and ultimately rate cuts by the European Central Bank are all helping to drive slightly better growth in 2026 and 2027 as well,” she says.

Will European stocks outperform those in the US?

In the last 15 years, large European companies have pivoted toward the American market. The proportion of STOXX 600 companies’ assets that are in the US has increased from 18% in 2013 to 30% in 2025, while around a quarter of STOXX 600 companies’ sales now come from the US.

“That’s a lot of dollar exposure,” Bell says. “What does all this mean for our strategy? We think this means we’ll see a little bit more diversification away from dollar exposure,” which could benefit European assets, she adds.

The outlook for European utilities in 2025

Utility stocks have rallied this year as the threat of US tariffs and concerns over a recession drove investors towards defensive stocks (companies which provide something that is likely to be in demand, regardless of the economic conditions).

European utility companies rose 20% relative to Europe’s STOXX 600 index in March alone.

Alberto Gandolfi, head of European utilities research, says that signs of increasing demand for power could be driving the outperformance of European utilities. Power demand so far in 2025 is up 1% in Germany, 1.5% in Italy, and around 4% in Spain, he says.

“Inflecting power demand is monumentally important, because it’s been declining for 15 years. This is completely changing the outlook for topline growth in the industry,” Gandolfi says.

To gauge whether the strong outperformance of European utilities is likely to continue, Gandolfi’s team has analyzed how the sector performed in previous crises, including the bursting of the dotcom bubble, the 2019 tariffs, and the Covid pandemic. They found that utilities normally outperform other stocks by around 10-30% during periods of market stress.

“Usually, you’re towards the top end of that range if two conditions are met: falling rates and a prolonged bear market. For utilities to continue to do as well as they’ve done in March and April, we would look for those features,” Gandolfi says.

Is it a good time to invest in European real estate stocks?

Real-estate stocks have also outperformed the broader STOXX 600 index throughout April. Jonathan Kownator, head of European real-estate research, attributes this to a combination of lower bond yields, the defensive nature of the sector, and discounted valuations for real estate stocks before the announcement of “reciprocal” tariffs by the Trump administration.

The average European real-estate stock trades below 14x price/earnings (compared with about 15x for the broader Stoxx 600 Index and around 25x for the US’s S&P 500 Index, as of May 15). “We’re looking at historically low valuations for the space as a result of the significant underperformance of real estate,” Kownator explains.

He adds that a high correlation with real bond yields suggests the sector is still too discounted, not even factoring in the solid European rental growth the team forecasts.

Kownator also points out that domestic real estate doesn’t have a first-order tariff impact, because it faces the European market.

“Within our space, thinking about the areas that have received more interest, and where we see the most resilience, German residential real estate comes to mind,” Kownator says, adding that this sub-sector is also the most sensitive to interest rates, and so it could benefit from future rate cuts.

The outlook for UK supermarket stocks

In the retail sector, there could be opportunities among grocers, and in UK food-retail stocks in particular, says Richard Edwards, head of Europe consumer research. Strong inflation, a growing population, and a broad shift from eating out to eating at home all make the UK a particularly attractive market for investors in this sector, he says. Edwards adds that the incumbents in the UK grocery sector are investing heavily in their own operations in response to pricing pressure from smaller retailers trying to grow their market share by lowering prices.

He points to strategies like everyday low pricing (as opposed to irregular sales or promotions), loyalty schemes, and price matches as ways that incumbents can keep investing in consumers to retain their custom. The result is that profitability has taken a hit across the board, but Edwards believes that grocers will return to growth next year.

“There are plenty of levers for these businesses to continue to offer really good value for the consumer, which is why I think this is something of a speed bump, rather than anything more fundamental than that,” Edwards says.

The UK’s four biggest grocery stores all saw an increase in grocery spending growth in April, due in part to a later than usual Easter. UK food retail sales were up 4.5% through March and April.